INTRODUCTION

Fundraising is a strategic exercise for any business and is not merely a question of obtaining capital. It is a critical component of corporate growth, expansion, and long-term sustainability. In Malaysia, fundraising activities are governed by a comprehensive regulatory framework administered primarily by the Securities Commission Malaysia (“SC”), Bank Negara Malaysia (“BNM”), Bursa Malaysia and the Companies Commission of Malaysia (“SSM”). The principal legislation regulating fundraising activities includes the Companies Act 2016 (“CA 2016”), Capital Markets and Services Act 2007 (“CMSA 2007”), Financial Services Act 2013 (“FSA 2013”) and Islamic Financial Services Act 2013 (“IFSA 2013”).

The selection of an appropriate fundraising method depends on various factors, including the company’s stage of growth, operational model, industry sector, risk profile, cash flow position, governance structure, and long-term strategic objectives. For the purpose of this article, we will be discussing on Malaysia’s fundraising ecosystem that can be categorised as equity-based fundraising, debt-based fundraising, capital market instruments, alternative financing platforms, digital asset and token-based, and strategic and ecosystem-based funding.

A. FUNDRAISING TOOLS

1. EQUITY-BASED FUNDRAISING

1.1 Share Issuance

One of the most traditional fundraising tools in Malaysia is equity financing through the issuance of shares. Under the CA 2016, companies limited by shares may issue ordinary shares or preference shares to investors in exchange for capital contributions. Equity financing allows companies to obtain long-term funding without repayment obligations because investors become shareholders in the company. However, the issuance of new shares dilutes the ownership and voting rights of existing shareholders. In practice, equity financing is generally suitable for start-ups, high-growth companies and businesses requiring substantial expansion capital.

1.2 Angel Investors

Angel investment refers to investments made by high-net-worth individuals into early-stage companies in exchange for equity participation. Angel investors typically provide seed funding to start-ups that may not yet qualify for bank financing due to limited operating histories or lack of collateral. In Malaysia, angel investment activities are supported through the Angel Tax Incentive introduced by the Government and administered by Cradle Fund Sdn. Bhd. where it aims to encourage qualified individual investors to invest in early-stage technology companies in Malaysia. Meanwhile, the accreditation body for angel investors and angel investor clubs in Malaysia is governed by the Malaysian Business Angel Network (“MBAN”), which oversees the registration and recognition of angel investors and structured angel investment groups. In practice, angel investment activities in Malaysia are facilitated through recognised networks such as MBAN itself, BizAngel Network, and regional platforms like the Sarawak Business Angel Network (“SBAN”), which connect accredited investors with early-stage start-ups and support structured investment syndication. Angel investment is particularly suitable for technology start-ups, fintech companies and innovative SMEs. The primary advantage of angel investment is that founders benefit not only from capital injection but also mentorship, networking opportunities and strategic guidance from experienced investors.

1.3 Venture Capital and Private Equity

Venture capital (“VC”) financing refers to investments made by professional investment firms into typically early-stage, high-growth companies with scalable business models, where VC investors provide funding in exchange for equity participation and often play an active role in governance and strategic decision-making. On the other hand, private equity (“PE”) financing generally targets more mature businesses with stable financial performance and expansion objectives. The SC recognises venture capital and private equity as important components of Malaysia’s capital market ecosystem. VC and PE investors commonly obtain equity ownership, governance rights and exit rights in exchange for their investments. Although these financing mechanisms provide access to substantial capital and strategic expertise, founders may experience dilution of ownership and reduced control over business decisions.

2. DEBT-BASED FUNDRAISING

2.1 Bank Financing

Traditional bank financing remains one of the most widely used fundraising tools in Malaysia. Commercial banks and Islamic banks provide facilities such as term loans, overdrafts, revolving credits, trade financing and asset financing. While debt financing is generally suitable for businesses with stable revenue streams, sound financial records and established credit profiles, Malaysian SME financing has evolved to include government-supported credit enhancement mechanisms that enable access to partially secured or unsecured financing. In particular, institutions such as the Credit Guarantee Corporation Malaysia Berhad (“CGC”) and Syarikat Jaminan Pembiayaan Perniagaan Berhad (“SJPP”) provide credit guarantee schemes that enable participating financial institutions to extend financing even to SMEs with insufficient collateral, by transferring part of the credit risk to the guarantor. These mechanisms are further complemented by BNM’s SME Fund, which channels subsidised financing through participating financial institutions to enhance access to affordable business financing across economic sectors. The principal advantage of debt financing remains the preservation of ownership control, as companies are able to raise capital without equity dilution. However, borrowers remain legally obligated to comply with repayment schedules, financing covenants and interest obligations imposed by financial institutions.

2.2 Revenue-Based Financing

Revenue-Based Financing (“RBF”) is a financing structure where investors provide capital to businesses in exchange for a percentage of the company’s future revenue until a predetermined repayment amount is achieved. Unlike traditional loans, RBF repayments fluctuate in line with the company’s revenue performance, while unlike equity financing, investors generally do not obtain ownership rights or voting control in the business. In Malaysia, RBF has recently been introduced and expanded as part of micro, small and medium enterprises (“MSMEs”) financing initiatives in scaling their businesses without equity dilution or collateral-heavy requirements.

RBF is particularly suitable for MSMEs and growth-stage businesses with recurring or predictable revenue streams, such as digital businesses, subscription-based models, and e-commerce enterprises, that require growth capital without significant shareholder dilution. Although Malaysia does not currently have standalone legislation specifically regulating revenue-based financing, such arrangements remain subject to contractual principles, the CA 2016, and applicable financial regulations depending on the structure of the transaction. One of the main advantages of RBF is the flexibility of repayment obligations, as repayments adjust according to business performance and cash flow capacity. However, MSMEs with unstable or declining revenues may experience longer repayment periods and higher overall financing costs over time, depending on revenue performance and contractual terms.

2.3 Convertible Notes

Convertible notes are hybrid fundraising instruments where investors initially provide financing in the form of debt that may subsequently be converted into equity upon the occurrence of specified events, such as future fundraising rounds or agreed conversion triggers. In Malaysia, the SC has introduced regulatory flexibilities to facilitate the issuance of convertible notes and convertible loan stocks to venture capital and private equity investors. Convertible instruments are particularly suitable for early-stage start-ups where company valuation remains uncertain and future financing rounds are expected. Their primary advantage lies in enabling companies to defer valuation negotiations while accessing early capital efficiently, thereby reducing transaction complexity in seed-stage fundraising. Although convertible instruments are not governed by a standalone legislative framework, their issuance is generally subject to the CA 2016, the CMSA 2007 (where applicable), and contractual principles under Malaysian law.

3. CAPITAL MARKET FUNDRAISING

3.1 Initial Public Offerings (“IPO”)

An Initial Public Offering (“IPO”) refers to the process whereby a private company offers its shares to the public for the first time and becomes listed on a stock exchange. In Malaysia, IPOs are regulated by the SC and Bursa Malaysia under the CMSA 2007 and the Bursa Malaysia Listing Requirements. Bursa Malaysia operates three primary markets, namely the Main Market, ACE Market and LEAP Market. The Main Market is intended for established corporations with strong profitability and operational track records, while the ACE Market caters to growth-oriented companies with expansion potential. The LEAP Market was introduced specifically to facilitate SMEs in accessing the capital market with comparatively lighter regulatory requirements. IPO fundraising is particularly suitable for companies seeking substantial expansion capital, enhanced corporate visibility and broader access to institutional and public investors. According to Bursa Malaysia, beyond raising capital, IPOs also enable companies to strengthen corporate profile, improve credibility and create long-term growth opportunities. However, listed companies are subject to stringent disclosure obligations, corporate governance standards and continuous compliance requirements imposed by the SC and Bursa Malaysia.

4. ALTERNATIVE FINANCING PLATFORMS

4.1 Equity Crowdfunding

Equity Crowdfunding (“ECF”) enables companies, particularly small and medium enterprises (“SMEs”) and start-ups, to raise funds from multiple investors through online platforms in exchange for equity ownership in the company. ECF was formally introduced and regulated in Malaysia by the SC in 2015 as part of its initiative to broaden access to capital markets under the framework of Recognised Markets and to provide alternative financing avenues for SMEs and start-ups that face challenges in obtaining traditional financing from banks and capital markets. The regulatory framework requires ECF platform operators to be registered as Recognised Market Operators (“RMOs”) with the SC and to comply with ongoing governance, disclosure, and investor protection requirements. ECF is particularly suitable for start-ups, SMEs, and consumer-focused businesses seeking both capital injection and market validation, as fundraising campaigns are conducted publicly through licensed platforms. However, issuers are required to comply with stringent disclosure obligations, including business information, financial disclosures, and risk statements, as mandated by the SC framework and platform operators. This ensures investor protection and market transparency while facilitating access to early-stage capital. Examples of SC-recognised ECF platforms in Malaysia include pitchIN and Mystartr.

4.2 Peer-to-Peer (“P2P”) Financing

Peer-to-Peer (“P2P”) financing is a debt-based fundraising mechanism where investors provide funds to businesses through online platforms, with repayment made together with an agreed return over a specified period. Similar to ECF, P2P financing operates via regulated digital platforms under the supervision of the SC, but differs in that it does not involve equity ownership. The SC introduced the P2P financing framework in 2016 under the Guidelines on Recognised Markets to broaden access to financing for SMEs and promote financial innovation. Platform operators must be registered as RMOs and comply with regulatory requirements on governance and investor protection. P2P financing is suitable for SMEs requiring working capital, invoice financing, and short-term funding, offering faster approval and lower collateral requirements compared to traditional bank loans. However, borrowers remain legally obligated to repay the financing amount with returns regardless of business performance. Examples of SC-registered platforms include Funding Societies Malaysia and CapBay.

5. DIGITAL ASSET AND TOKEN-BASED FUNDRAISING

5.1 Initial Exchange Offerings and Digital Tokens

Malaysia has introduced regulated digital asset fundraising mechanisms through Initial Exchange Offerings (“IEO”), which allow companies to raise capital through the issuance of digital tokens. A digital token generally refers to a digital representation of value or rights that is recorded and transferred electronically using distributed ledger or blockchain technology. The SC introduced the regulatory framework for digital asset fundraising under the Guidelines on Digital Assets to facilitate alternative fundraising while ensuring investor protection and market integrity. Under the IEO framework, issuers offer digital tokens to investors through SC-registered IEO platform operators, who act as intermediaries responsible for conducting due diligence on the issuer, assessing the viability of the proposed project, and reviewing disclosures contained in the issuer’s whitepaper before the token offering may be launched. Investors who participate in the IEO subscribe to the digital tokens through the platform, and the funds raised are channelled to the issuer for project development or business expansion. IEOs are particularly suitable for blockchain-based companies, fintech businesses and technology ventures involving digital ecosystems or utility-driven digital platforms. Although Malaysia adopts a progressive regulatory approach towards digital assets, digital token investments remain highly speculative and are subject to regulatory, cybersecurity, technology and market volatility risks.

6. STRATEGIC AND ECOSYSTEM-BASED FUNDING

6.1 Government-Backed Funding

The Malaysian Government provides funding support through grants, matching funds and soft loans administered by agencies such as Cradle Fund Sdn. Bhd., SME Corp Malaysia, Malaysia Digital Economy Corporation (“MDEC”) and the Malaysian Research Accelerator for Technology & Innovation (“MRANTI”). These schemes are primarily aimed at supporting SMEs, particularly in digitalisation, innovation and technology development aligned with national economic policies. Government grants are typically non-dilutive and do not require repayment, making them attractive for early-stage and innovation-driven businesses. However, they are highly competitive and subject to strict eligibility criteria, documentation requirements and performance monitoring by the relevant agencies.

Malaysia also supports accelerator and incubator programmes as part of its startup ecosystem. Accelerators are structured, time-bound programmes offering funding, mentorship and market access, while incubators focus on longer-term business development support. These programmes may provide funding through grants, equity or strategic partnerships and are particularly suitable for technology-driven start-ups seeking early-stage capital and ecosystem support.

7.1 Joint Ventures (“JV”)

A joint venture (“JV”) refers to a commercial arrangement where two or more parties agree to combine resources, expertise, capital or business operations for a specific commercial objective. In Malaysia, joint ventures are commonly structured through incorporated joint venture companies or contractual arrangements governed by shareholders’ agreements and joint venture agreements. Although joint ventures are not traditionally categorised as direct fundraising instruments, they may function as strategic financing mechanisms because parties to the joint venture may contribute capital, assets, intellectual property, technology or operational expertise into the venture. Joint ventures are therefore commonly used to facilitate large-scale infrastructure projects, property developments, foreign investments and technology collaborations. Joint ventures are particularly suitable for companies seeking strategic partners, risk-sharing arrangements, market access or additional project financing capacity. One of the primary advantages of joint ventures is the sharing of financial risks and operational resources between parties. However, joint ventures may also create governance challenges, management disputes and conflicts relating to profit-sharing or decision-making authority.

Overall, Malaysia provides a comprehensive and well-regulated fundraising ecosystem covering equity, debt, alternative financing platforms, and emerging digital asset instruments. It is overseen by the SC, BNM, Bursa Malaysia, and the SSM, ensuring investor protection, market integrity, and corporate accountability. Companies must therefore assess their funding needs, objectives, compliance capacity, and risk exposure when selecting suitable financing tools.

Fundraising readiness is also closely linked to proper legal housekeeping, including maintaining accurate corporate records, financial statements, shareholder registers, and compliance documents, which are essential for due diligence during financing applications. This leads to the importance of legal housekeeping as a key foundation supporting successful fundraising in Malaysia.

B. LEGAL HOUSEKEEPING FOR ALL MALAYSIAN BUSINESSES

Before a target company is considered for investment or admitted into a fundraising round, investors will typically require a due diligence exercise to be conducted. This may take the form of legal, financial, or tax due diligence, and is intended to provide a clear understanding of the company’s overall health, compliance status, and growth potential. In practice, however, many businesses only begin to organise their records and documentation once investors initiate this process. While larger companies may already have established bookkeeping systems, secretarial support, and internal standard operating procedures, many SMEs and growth-stage businesses often operate with informal arrangements, undocumented understandings, or incomplete statutory records.

Legal housekeeping is therefore essential because it ensures that a company’s corporate, contractual, and regulatory affairs are properly maintained and accurately reflected, allowing investors, banks, buyers, and strategic partners to rely on the information presented without requiring extensive reconstruction or remediation. Due diligence is conducted by these parties not merely as a procedural requirement, but as a risk assessment tool to verify ownership, assess legal exposure, confirm financial integrity, and evaluate whether the business is capable of sustaining and scaling operations once funds are injected. In more severe cases, where there is a significant lack of documentation or the due diligence outcome is materially unsatisfactory, such deficiencies may result in downward valuation adjustments, the imposition of enhanced investor protections (such as stronger warranties, indemnities, or escrow arrangements), or, even to the extent of withdrawal of the investor and termination of the proposed transaction altogether.

Corporate legal housekeeping is often one of the most critical aspects assessed during a due diligence exercise. While businesses frequently focus on revenue growth and operational expansion, investors, financiers, and strategic partners are equally concerned with whether the company has been properly structured, managed, and maintained from a legal and compliance perspective. In many cases, deficiencies identified during due diligence do not necessarily relate to the viability of the business itself, but rather to the lack of documentation, inconsistent governance practices, or unresolved regulatory and operational issues accumulated over time.

At its core, legal housekeeping involves ensuring that the company’s corporate records, contractual arrangements, regulatory compliance, and operational documentation are properly maintained, accurate, and readily verifiable. This includes maintaining updated constitutional documents, shareholders’ agreements, board and shareholders’ resolutions, statutory registers required under the CA Act 2016, beneficial ownership records, and proper documentation relating to the issuance, allotment, and transfer of shares. Investors will generally expect the company’s corporate records to accurately reflect the actual operational and ownership structure of the business, particularly where external funding is being introduced.

One area that frequently becomes problematic during fundraising is the target’s capitalization table hygiene. Many growing businesses begin with informal arrangements among founders, friends or family members, which may later become difficult to reconcile during due diligence. Common issues include undocumented nominee arrangements, oral promises of equity, founder disputes, unclear vesting arrangements, undocumented convertible instruments, or poorly implemented employee share option schemes (ESOS). While such arrangements may initially arise out of convenience or trust, they often create uncertainty regarding ownership, control, dilution, and investor rights, all of which are key considerations for incoming investors.

Regulatory compliance is another significant component of legal housekeeping. Businesses are often under the impression that compliance is limited to annual filings with the SSM, when in reality the scope of compliance may extend far beyond corporate secretarial matters. Depending on the nature of the business, companies may also be subject to sector-specific regulatory frameworks, licensing requirements, employment obligations, anti-money laundering controls, personal data protection requirements, and industry-specific operational approvals. Accordingly, due diligence exercises are rarely uniform and are typically tailored to the business activities and risk profile of the target company.

For example, companies operating regulated businesses under the oversight of the Bank Negara Malaysia or the Securities Commission Malaysia are generally subjected to significantly more stringent due diligence processes. In such cases, investors and financiers will not only review the company’s corporate records, but will also assess licensing conditions, regulatory approvals, internal governance frameworks, compliance policies, reporting obligations, operational controls, anti-money laundering and counter-financing of terrorism (AML/CFT) measures, and historical regulatory correspondence. Regulatory compliance for licensed entities therefore extends far beyond standard corporate compliance under the CA 2016.

Similarly, the scope and focus of due diligence may differ substantially depending on the underlying nature of the business itself. For businesses involved in plantation, such as palm oil operations, their due diligence may place greater emphasis on environmental impact, sustainability compliance, land ownership, land use rights and operational permits attached to the land or business activities. In contrast, for technology companies, greater focus is typically placed on intellectual property ownership of proprietary technology, software development arrangements, data protection compliance, and cybersecurity measures of the target.

Apart from regulatory matters, commercial contracts also form a key component of legal housekeeping. Businesses should ensure that material customer agreements, supplier arrangements, distribution agreements, SaaS or platform terms, employment contracts, confidentiality provisions, and intellectual property ownership clauses are properly documented and enforceable. During due diligence, investors will often assess whether key operational relationships are sufficiently protected contractually, whether revenue streams are legally secured, and whether any material contractual risks could affect the continuity or profitability of the business.

Ultimately, effective legal housekeeping is not merely an administrative exercise but a critical component of investment readiness and operational sustainability. Businesses with clear governance structures, proper documentation, strong compliance practices, and organized records are generally better positioned to navigate due diligence processes efficiently, inspire investor confidence, and minimize transactional delays or disputes during fundraising exercises.

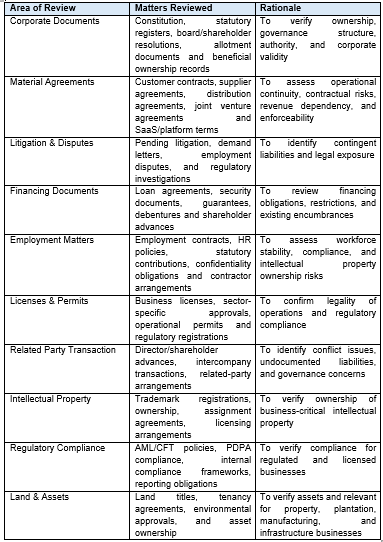

Below is a general overview of the categories and documents commonly reviewed during a due diligence exercise:

Legal housekeeping should not be viewed purely as a reactive exercise conducted only when investors request due diligence. Instead, businesses should implement practical governance, compliance, and documentation systems early in their lifecycle to improve operational discipline and transaction readiness.

One of the most practical tools businesses can establish is a centralized due diligence data room. A properly maintained data room allows the company to organize and store key corporate, financial, operational, and regulatory documents in a structured manner, significantly reducing time and inefficiencies during fundraising or transaction exercises. Businesses with organized records are generally able to respond more efficiently to investor requests and project stronger governance maturity.

Companies should also maintain internal compliance trackers and corporate calendars to monitor key filing deadlines, licensing renewals, board approvals, and statutory obligations. This is particularly important for regulated businesses operating under ongoing reporting and compliance requirements.

Contract management systems may similarly assist businesses in organizing customer agreements, supplier contracts, employment documents, and material commercial arrangements. In many growing businesses, operational agreements are often scattered across emails, unsigned drafts, or individual departments, making document retrieval difficult during due diligence.

From a governance perspective, businesses should also consider implementing board approval matrices, delegated authority frameworks, conflict management procedures and internal reporting structures.

For startups and growth-stage businesses, implementing standardized template employment agreements, confidentiality clauses, intellectual property assignment provisions, and commercial agreements can also significantly reduce future legal uncertainty.

One of the most common mistakes businesses make is waiting until investors, financiers, or purchasers initiate due diligence before attempting to organize their corporate and legal affairs. In reality, legal housekeeping is most effective when implemented proactively from the early stages of the business, ideally from incorporation or before significant expansion occurs.

By the time a fundraising exercise begins, businesses are often operating under tight timelines, investor pressure, and transaction demands. Attempting to reconstruct years of missing records, undocumented arrangements, incomplete approvals, or unclear ownership structures during this period can become time-consuming, expensive, and disruptive to the transaction process.

Importantly, legal housekeeping is also significantly cheaper and easier to implement before disputes, regulatory issues, or fundraising complications arise. Preventive governance and documentation practices are often far less costly than corrective restructuring exercises conducted during active transactions or disputes.

As fundraising and transaction environments become increasingly sophisticated, investors, financiers, purchasers, and regulators are placing greater emphasis not only on profitability and growth potential, but also on governance quality, transparency, compliance discipline, and operational maturity. Businesses with organized records, proper governance frameworks, clear ownership structures, and well-maintained compliance systems are generally able to navigate due diligence exercises more efficiently and inspire greater confidence among stakeholders.

CONCLUSION

In conclusion, Malaysia offers a diverse and well-regulated fundraising ecosystem encompassing traditional financing, alternative platforms, government support schemes, and emerging digital asset mechanisms, enabling businesses to access capital at different stages of growth. However, access to these funding avenues is closely dependent on a company’s legal and operational readiness. Effective legal housekeeping, through proper corporate records, contractual documentation, regulatory compliance, and governance practices, plays a critical role in facilitating smooth due diligence processes and enhancing investor confidence. As such, fundraising capability and legal housekeeping are interdependent, and businesses that maintain strong documentation and compliance discipline are better positioned to secure financing efficiently and support long-term sustainable growth.

Published Date: 13 May 2026

Authors:

- Maryam Amilah Zaini

- Fadhlil Azim