Setting Up Family Office in Labuan International Business and Financial Centre (“Labuan IBFC”)

The rise in Asia’s economy has left a great demand for customized financial services. As a result, Family Offices[1] (“FOs”) is the preferred option for managing the intricate financial requirements of high net-worth individuals[2] (“HNWIs”) and ultra-high net-worth individuals[3] (“UHNWIs”), including investment management, tax and estate planning, philanthropy and family governance. The Exposure Draft of Guidance Notes on the Establishment of Family Office in Labuan IBFC[4] dated 26 July 2024 (“Guidance Notes”), intended to serve as a framework in facilitating the establishment of FOs through Labuan IBFC, has shed light on the practical aspects of FOs including clarity on the available structures and regulatory incentives. In this article, we explore the various structures of FOs offered by Labuan IBFC, highlighting their key features, benefits and drawbacks while also comparing them with FOs under Forest City Scheme.

Key Features

The attractiveness of FOs in Labuan stems from the following key features of Labuan IBFC, along with the flexibility provided through its Guidance Notes:

- Diverse range of wealth management vehicles offered by Labuan IBFC including private trust companies and foundations, catering to both common law and civil law jurisdictions.

- Labuan IBFC’s ability to provide both conventional and Shariah-compliant structures such as Islamic trusts, Islamic foundations and waqf foundations.

- The flexibility granted to FOs to co-locate anywhere in Malaysia, allowing businesses to tailor their operations to their strategic goals.

FO Structures in Labuan IBFC

With its diverse range of business structures, Labuan IBFC offers a variety of wealth management solutions tailored for establishing FOs, providing the essential features that affluent families require. Below are the different structures available through Labuan IBFC:

- Labuan Holding Company (“LHC”)

- Labuan Protected Cell Company (“LPCC”)

- Foundation

- Trust

- Private Trust

Building on the above, different types of structures can be integrated when establishing a FO, allowing for the optimization of wealth management for affluent families.

Comparison of FO structures available

With the wide array of options available, businesses naturally seek to choose the most suitable structure for their operations. To assist in this decision-making process, the diagram below is designed to help businesses and affluent families identify the optimal structure for their needs.

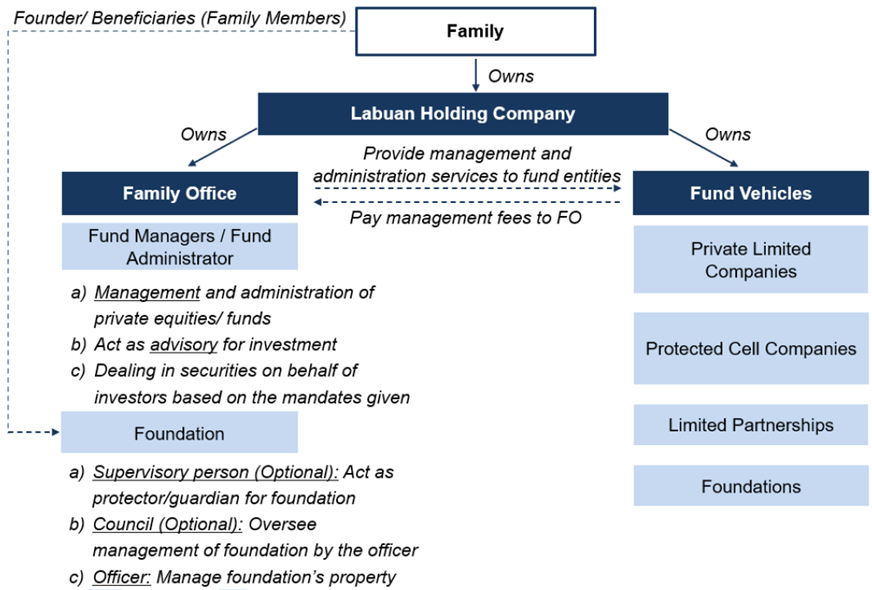

| 1. FO structured through a LHC

Diagram from the Guidance Notes |

||

| Design | Benefits | Drawbacks |

| Central entity managing the Family Office, investment portfolios, and providing administrative services to associated entities (trading companies, fund managers, foundations, private trusts). | Efficiently manage everything under one roof with streamlined operations, clear oversight, aligned investment goals, and a unified structure that supports a variety of investments. | · May be complex to manage depending on the number of associated entities.

· Requires coordination across multiple entities, which may add to operational costs. |

| 2. FO structured through a LHC and LPCC

Diagram from the Guidance Notes |

||

| Design | Benefits | Drawbacks |

| Allows the creation of multiple “cells” within a single legal entity, each with separate assets and liabilities. | · Provides strong asset protection; one cell’s liabilities cannot affect others.

· Flexibility to pursue different investment strategies within separate cells. · Facilitates risk management by isolating portfolios. |

· Complexity in managing multiple cells.

· Compliance and governance must be observed for each cell independently. · Initial setup costs may be high. |

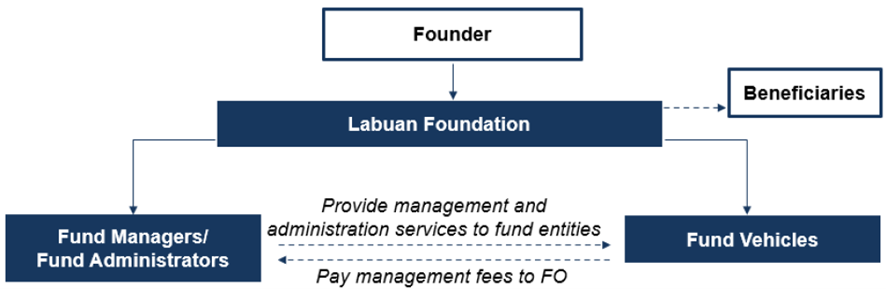

| 3. FO structured using Labuan Foundation

Diagram from the Guidance Notes |

||

| Design | Benefits | Drawbacks |

| A legal structure where the founder transfers assets to manage and protect for designated beneficiaries, such as shares in fund managers or investment vehicles. | · Allows for smooth intergenerational wealth transfer.

· Provides flexibility in overseeing wealth distribution and preservation. · Legal governance ensures adherence to the founder’s wishes. |

· Requires careful governance to ensure compliance with legal and regulatory requirements.

· May limit operational flexibility for more dynamic investment activities. |

| 4. FO structured using Labuan Trust

Diagram from the Guidance Notes |

||

| Design | Benefits | Drawbacks |

| A legal arrangement where the Settlor transfers assets to a trust, which may be structured for discretionary wealth management or charitable endeavors, compliant with Shariah principles if required. | · Highly flexible structure, especially for wealth management or charitable purposes.

· Can be structured for Shariah compliance. · Protects assets from personal liabilities of beneficiaries. |

· Requires a formal written instrument for creation.

· Trust structures can be more complicated and require legal and administrative oversight. · High costs for setting up and maintaining a trust structure. |

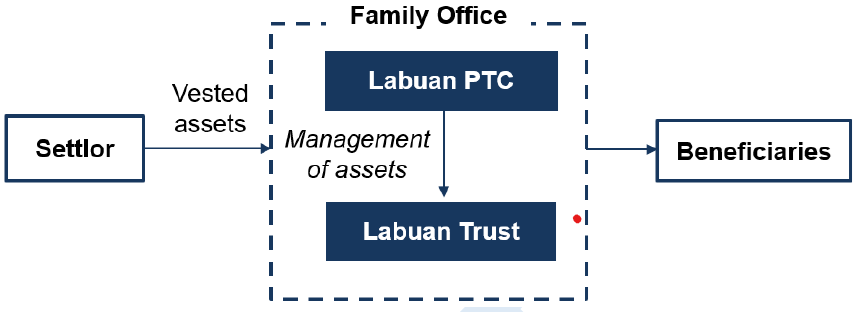

| 5. FO structured using Labuan Private Trust Company

Diagram from the Guidance Notes |

||

| Design | Benefits | Drawbacks |

| A private trust company created to administer a family-owned trust, offering customized governance and wealth management strategies. | · Allows families to control estate planning and succession management.

· Cost-effective in the long term for managing large family estates. |

· High initial setup costs.

· May require more involvement from family members in trust administration. · Not ideal for smaller estates due to the complexity and costs involved. |

Comparison with the Forest City Scheme

The Malaysian government’s initiative to enhance the investment landscape has also resulted in the introduction of the Single-Family Office[5] (“SFO”) Scheme, which provides a concessionary tax rate of 0% on income generated from eligible investments within the scheme. The Securities Commission (“SC”) is tasked with overseeing this initiative, which will initially be implemented in Forest City[6]—the first location in Malaysia to offer such attractive investment incentives. To qualify for the incentive, Single Family Office Vehicles[7] (“SFOVs”) must meet several conditions, including establishing a registered office in Pulau 1, Forest City, holding assets under management (AUM) of at least RM30 million, and employing investment professionals. For comparison, the table below outlines the key differences and advantages between FO in Forest City Scheme and Labuan IBFC:

| Aspect | Forest City Scheme | Labuan Family Office Services |

| Tax Incentive | 20-year tax incentive (split into two 10-year periods), 0% tax rate | Tax-efficient but not 0%, depends on structure |

| Legal & Regulatory Framework | Relatively new, expected operational by early 2025 | Well-established, robust legal and regulatory framework |

| Wealth Management Options | Centralized, tax-efficient management | Comprehensive, tailored wealth management (asset protection, risk management, multi-generational planning) |

| Type of FO | SFOs only | SFOs and Multi-Family Offices |

| Focus | Tax incentives for high-net-worth families | Tailored, diversified solutions for wealth management |

| Flexibility | More restrictive due to location and requirements | High flexibility, can operate based on family’s strategy |

Conclusion

In conclusion, families seeking comprehensive and flexible wealth management solutions will most likely lean towards Labuan IBFC. With its well-established regulatory framework and diverse structures, it caters to complex financial needs. This includes asset protection, multi- generational planning and Islamic-compliant operations. Ultimately, Forest City Scheme may also appeal to families who are focused on tax incentives and centralized management. We find that both schemes provide valuable opportunities and the decision falls back to the family’s specific financial objectives in the long run.

Authors:

- Fakhrullah Fadzilah

- Wan Tasnima

References:

[1] Typically, the threshold for establishing a family office is at least USD250 million in investible assets.

[2] Individuals with liquid assets of at least USD1 million.

[3] Individuals with a net worth of at least USD30 million.

[4] To be issued pursuant to Section 4A of the Labuan Financial Services Authority Act 1966 (LFSAA).

[5] Typically, a corporate entity wholly owned by one or more individuals from the same family, established to manage the family’s investments.

[6] A man-made island located just across the Johor strait, in sight of Singapore.

[7] Typically, a corporate entity wholly owned by one or more individuals from the same family, established to manage the family’s investments.